Recently we have mentioned two new trades for The Tail Chaser's portfolio:

(A) Short EURBRL @ 2.3913 spot reference, 20% of NAV

(B) Receiving BRL DI Futures @ 10.89%, 300% of NAV

Drivers:

(A) There WAS a resistance around 2.40-spot and the USDBRL was exploding upwards. The carry is still very interesting, 54bp/month. Europe has a very serious debt problem, with periphery yields creeping higher even with the ECB pumping lots of cash into buying these issues. Banks will soon start to come to the surface with holes in their balance sheets while local politicians don't understand the severity of the big picture. AND I like some of the long-term BRL fundamentals like demographics, room for productivity growth, exposure to raw materials [especially food-related], room to cut interest rates to fuel economic growth and credit growth, etc.

BUT....

I have forgotten the reason I closed out the Short Ibovespa / Short USDBRL and the other Currency Basket trade: the IOF tax on new BRL longs through derivatives and the consensus 'We love Brazil' mood.

Opening Monday, following the trade executed last friday, the cross was already sky rocketing, and from there it only looked worse.

Looking at the stand-alone trade it was a case for getting out right away: BRL in a horrible momentum and the clear stop-price above the 2.40 resistance was broken EASILY. Like butter. But I stepped back and looked at the overall portfolio and decided to wait and see for a little longer.

In two days the Brazilian Central Bank called an FX auction and sold USD2bln+ into the market helping damp volatility and signalling to the market they were not just sitting, but watching and acting. And in the mean time the EUR started to drop a bit vs many currencies.

So... now I am more comfortable holding the position and, at 20% of the NAV, and me having an overall bearish portfolio, I am more comfortable with it.

(B) Receiving 300% of NAV in Jul12 BRL DI Futures: The Brazilian Central Bank has shown remarkable courage in reversing course in monetary policy on the last metting at the end of August even with current inflation very high. Allied with the Finance Ministry and the President, the BCB's speech has been very dovish. They sound like a hedge fund calling out market turmoil, heightened volatility and darker days ahead, a view that I share. That's very significant if coming from policy makers. After the equity markets tumbled this week, with commodities down considerably and currencies getting shattered against the USD and JPY I thought it was time to believe the BCB meant what he was saying. Using the panic in the local rates market, when pricing was of reduction in the overall size and length of rate cuts, probably because of people getting out of the local bond markets, I sold into the strength betting there's is a greater chance of larger cut in October, the world would collapse, inflation expectations in Brazil would decrease and the strong hand of the BCB on the USDBRL market would dampen volatility and improve its image with investors.

That's it.

Current positions:

~200% of NAV in Germany Dec16 CDS

~100% of NAV in May14 USDCNY 6.80 calls

~300% of NAV receiving Jul12 BRL DI Futures

~20% of NAV short EURBRL

~100% of NAV long JPY Swaption Payers, strike 4%, March 2014

~15% of NAV long Gold / short Silver (XAUXAG)

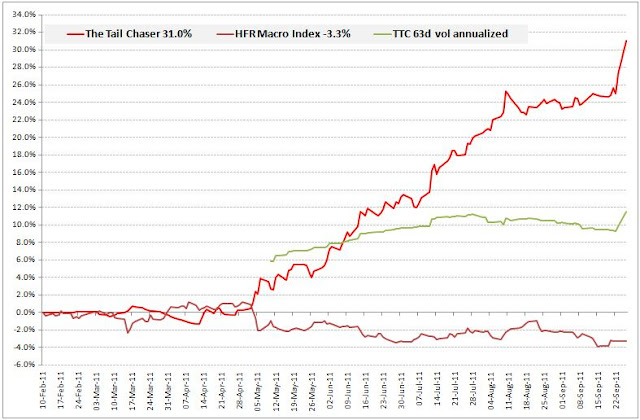

Some charts below...

(A) Short EURBRL @ 2.3913 spot reference, 20% of NAV

(B) Receiving BRL DI Futures @ 10.89%, 300% of NAV

Drivers:

(A) There WAS a resistance around 2.40-spot and the USDBRL was exploding upwards. The carry is still very interesting, 54bp/month. Europe has a very serious debt problem, with periphery yields creeping higher even with the ECB pumping lots of cash into buying these issues. Banks will soon start to come to the surface with holes in their balance sheets while local politicians don't understand the severity of the big picture. AND I like some of the long-term BRL fundamentals like demographics, room for productivity growth, exposure to raw materials [especially food-related], room to cut interest rates to fuel economic growth and credit growth, etc.

BUT....

I have forgotten the reason I closed out the Short Ibovespa / Short USDBRL and the other Currency Basket trade: the IOF tax on new BRL longs through derivatives and the consensus 'We love Brazil' mood.

Opening Monday, following the trade executed last friday, the cross was already sky rocketing, and from there it only looked worse.

Looking at the stand-alone trade it was a case for getting out right away: BRL in a horrible momentum and the clear stop-price above the 2.40 resistance was broken EASILY. Like butter. But I stepped back and looked at the overall portfolio and decided to wait and see for a little longer.

In two days the Brazilian Central Bank called an FX auction and sold USD2bln+ into the market helping damp volatility and signalling to the market they were not just sitting, but watching and acting. And in the mean time the EUR started to drop a bit vs many currencies.

So... now I am more comfortable holding the position and, at 20% of the NAV, and me having an overall bearish portfolio, I am more comfortable with it.

(B) Receiving 300% of NAV in Jul12 BRL DI Futures: The Brazilian Central Bank has shown remarkable courage in reversing course in monetary policy on the last metting at the end of August even with current inflation very high. Allied with the Finance Ministry and the President, the BCB's speech has been very dovish. They sound like a hedge fund calling out market turmoil, heightened volatility and darker days ahead, a view that I share. That's very significant if coming from policy makers. After the equity markets tumbled this week, with commodities down considerably and currencies getting shattered against the USD and JPY I thought it was time to believe the BCB meant what he was saying. Using the panic in the local rates market, when pricing was of reduction in the overall size and length of rate cuts, probably because of people getting out of the local bond markets, I sold into the strength betting there's is a greater chance of larger cut in October, the world would collapse, inflation expectations in Brazil would decrease and the strong hand of the BCB on the USDBRL market would dampen volatility and improve its image with investors.

That's it.

Current positions:

~200% of NAV in Germany Dec16 CDS

~100% of NAV in May14 USDCNY 6.80 calls

~300% of NAV receiving Jul12 BRL DI Futures

~20% of NAV short EURBRL

~100% of NAV long JPY Swaption Payers, strike 4%, March 2014

~15% of NAV long Gold / short Silver (XAUXAG)

Some charts below...

*Disclaimer: charts and data are presented as I receive/see them. Sources are usually not checked for validation and my own calculations are of 'back of the envelope'-type. I am aware that some math that I do myself might be wrong and/or misleading to some extent. In financial markets the rate of change of economic data is often more important than the actual level and the perception of 'what is priced in' is more important than 'what is actually going to happen'. This is actually the way people pick entry and exit points. So... yes, sometimes you might say 'This guy is an idiot, this is way wrong!' with a high conviction, being right. Not to worry. Markets are made of expectations and the clash of conviction between its participants. Portfolio managers know that being an idiot is sometimes profitable and being smart is often a bad choice. It is all reality, sometimes good, sometimes bad. By the way: corrections to my analysis and intelligent debate is welcome. theintriguedtrader AT gmail do com

No comments:

Post a Comment